Risks and opportunities in 2025 will likely be driven by a few key macro themes emerging globally. Some of these we’ve discussed in prior years, whereas others are we are layering on as additional considerations.

We'll first identify these macro themes to help us better understand the expected state of the world. After discussing these themes, this report will dissect the emerging risk and opportunities we expect in the year ahead.

Three Macro Themes: World Order, Trade and Demographics

Theme 1: A Fracturing World Order

We’ve discussed this theme quite a bit but shifts in the global order will only accelerate in the coming year, influencing how nations interact with one another. And these changes could unfold in complex, nonlinear ways.

Let's look at India as an example, which will likely continue to be the fastest growing major economy with GDP expansion in excess of 7%. Within a few years, India will likely become the third largest economy after the U.S. and China. These newfound economic gains will translate into two overt shifts that could increase India’s geopolitical influence.

First, increased consumption and wealth within India could make it a bigger destination for foreign companies. Some firms, particularly in the technology space, will continue to shift their manufacturing base to India to avoid the deteriorating geopolitical environment between the U.S. and China.

Second, foreign policy will likely continue to sharpen as New Delhi seeks to leverage its economic heft to assert its interests. The goal of policymakers will be to maximize India’s friends and partnerships to ensure that India can elevate its position on the global stage and accrue as much economic gain as possible, while avoiding alliances or being drawn into conflicts and picking sides (e.g., remaining close to both the U.S. and Russia, while deepening a relationship with Israel and maintaining ties to Iran).

India’s economic rise will enable it to continue to carve out its own sphere of influence based upon its style of international engagement. China will likely continue to seek out a status as a regional, if not global, hegemon. Other rising economies in the region will likely aim to increase their influence through various conduits (i.e., Saudi Arabia finding new oil exporting markets while investing domestically in its economy).

Aside from the rising influence of India, ongoing macro themes could gain more prominence. The rise of the BRICS is one example. The BRICS are a bloc of nations that cooperate with each other on shared goals. They include Brazil, Russia, India, China, South Africa, and others. While the BRICS does not seek to rival the G7 or other multilateral forums, they are becoming increasingly cohesive and are unofficially seeking to challenge western dominance over the global economic and financial architecture.

As these nations grow their economic strength and deepen their geopolitical linkages, it will inevitably lead to a continued fracturing of the world order. As we know through history, when there are multiple power centers around the world, global friction increases. During the Cold War, there were two main power blocs aligned with the U.S. and the Soviet Union. Looking ahead. there could be many power blocs. Therefore, geopolitics will increasingly become complex and nuanced in the year ahead.

Theme 2: Shifts in Global Trade

Global trade will increasingly fragment due to a shifting world order. We do not believe globalization is ending, but it’s shifting.

China is expected to continue to focus on its manufacturing- and export-oriented economic model. Despite expectations that Beijing would seek to switch from exports to domestic consumption and services after reaching a middle-income level, that has not fully happened. Research suggests household savings rates in China remain elevated while consumption is not rising much. Policymakers will likely focus on government spending and exports to maintain growth, which means that China will continue to produce goods and send them around the world to offset a potential hard landing. But this economic model is increasingly at odds with the U.S. and some of its partners, which will seek to limit Chinese imports. At the end of the day, we have a situation where China will remain the world’s largest exporter and the U.S. the world’s largest consumer and importer.

Some companies will leave China and move to India or elsewhere to “simplify” their supply chain and avoid being caught up in geopolitical challenges. But in many cases, goods may simply be rerouted and either assembled or packaged in other markets, like Mexico, thereby contorting global trade. Think about what that means for the medium term. Suddenly, Mexico and China will become closer to one another given their trade and economic linkages. This points towards the fracturing order. Along the way, China will continue to accrue U.S. dollars via its exports. Its economic growth will likely slow, but overall Beijing will continue to seek dominance in its region and beyond.

Theme 3: Demographic Divergence Across Nations

Globally, the world population is not aging. In fact, the distribution of ages around the world is somewhat similar now as it was 70 years ago. But the population is aging quickly in some countries while remaining young in others. For example, in Germany roughly 30% of the population is under the age of 30, while 54% is between the ages of 30 and 70. The latter group will eventually retire, or has already retired, whereas the number of replacement workers will be fewer. China is also rapidly aging with 35% of the population under the age of 30, and 57% between 30 and 70. India, on the other hand, is very young in terms of its demographic split. Of the around 1.5 billion people in India, 70% were either born or came of age after 1990. More specifically, 53% of the population is under the age of 30 and 43% is between 30 and 70. For India, there are more potential future workers than retirees. For the US, the numbers are 39% under 30 and 50% between 30 and 70. Therefore, the US is not as “top-heavy” as Germany, but also not as “young” as India.

Aging societies create economic challenges when a small number of workers end up supporting a large number of retired citizens. There are fiscal costs to this structure, including higher government spending to support retirees, as well as headwinds to consumption and overall economic growth. The U.S. can address this—and has over the years—via immigration. For Europe and China, leveraging immigration to fill the demographic voids may be more challenging. Accordingly, growth in Europe and China may start to decelerate.

Another solution to the demographic challenges is the adoption of artificial intelligence to support economic growth and productivity. Hence why AI will likely emerge as the largest geopolitical flashpoint. The nation that can control AI is poised to dominate the global economy for the next five decades. Given that many nations have a demographic challenge that could become an economic headwind, dominating AI becomes even more important. AI could also enhance the military capabilities of various nations too.

Demographic Shifts Likely to Cause Labor Imbalances

Softening Expected in U.S. Job Market

In 2024, the U.S. labor market exhibited general strength, with some indications of loosening. To recap:

- 2020: The pandemic brought mass job losses and the unemployment rate peaked at 14.8%.

- 2021: Unemployment fell to 5.4% as the economy rebounded.

- 2022: The job market tightened with 12.2 million unfilled positions and the unemployment rate fell to 3.6%. Some of this was attributed to a section of society retiring and leaving the workforce.

- 2023: The unemployment rate increased slightly as individuals re-joined the job market and applied to unfilled positions.

- 2024: Conditions loosened a bit more and the unemployment rate trended above 4%.

As we head into the start of 2025, it’s evident that the labor market is moving closer to its pre-pandemic status quo. The ratio of open positions to available talent is almost back to the 1x to 1.2x range, roughly where it was just before the pandemic.

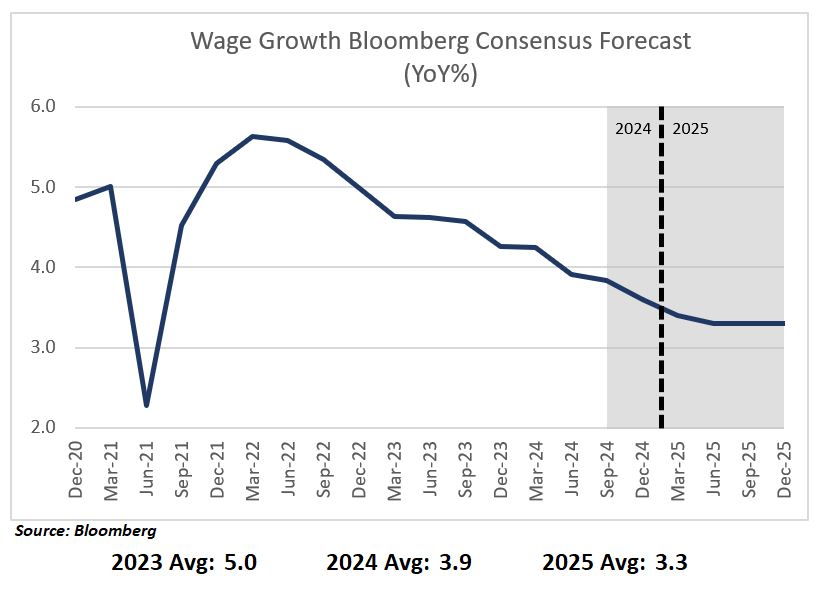

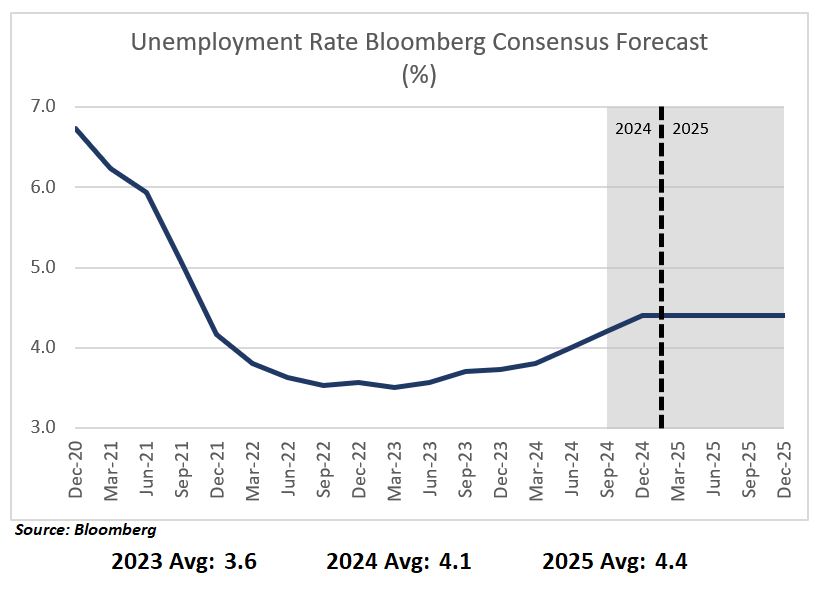

For the year ahead, the market consensus expects the U.S. economy to add on average 120,000 new jobs per month; the unemployment rate to average 4.4%; and for wage growth to average 3.3% year-over-year (also referred to as wage inflation).

The Global Insights Center is generally aligned with these expectations, though we expect a slightly higher unemployment rate and a potentially lower wage inflation figure.

We believe though that the job market will face ongoing challenges stemming from our aging society. A large share of the U.S. workforce is near retirement age, and the business community will lose some talent to retirements over the next decade. At the same time, it will be difficult for younger generations to backfill those positions given the rate at which retirements are expected. The younger population entering the workforce will barely offset retirements, limiting growth in the size of the overall workforce.

Due to the aging workforce, immigration trends will be important for job growth. Over the past few years, we believe that immigration helped ease labor shortages across many sectors. According to data from the Bureau of Labor Statistics, foreign-born individuals were responsible for all labor force growth in 2024, while the U.S.-born workforce declined. Put another way, the 2024 job market would have remained overly tight without an influx of immigrants, and labor shortages would have persisted in some sectors. This means the unemployment rate would have been lower, and wage inflation likely even higher. Therefore, immigration helped the job market expand while also putting it on a path back to pre-pandemic wage growth.

But in 2025, immigration could slow, thereby limiting the economy’s ability create and fill jobs. We say this based on data trends available from the U.S. Customs and Border Protection pointing towards a slowdown in immigration.

Employment and Wage Expectations Across Construction, Healthcare and Tech

Construction firms have faced staffing challenges over the past few years, putting upward pressure on wages, especially in the general contractor space. The construction sector added jobs faster than almost any other industry in 2024, and construction wages increased 4.9% YoY, outpacing the national average. Construction demand is expected to remain robust in 2025, whereas lower immigration will restrict labor availability. As a result, wages may see continued pressure in the construction sector, and construction wages could rise to $40.50 per hour in 2025, up 4.3% from the prior year.

Healthcare job growth was strong in 2024, led by hiring for home health aides and nursing center staff. Wage growth, on the other hand, was below average, at just 3.7%. These trends should continue in 2025, with job growth above 4% but wage growth below 3.5%. Across the sector, wage inflation is expected to be especially low for doctors, falling below 3%. Though it could be higher for home health aides and nursing home staff, exceeding 4.5%.

Trends in tech and biotech are heavily influenced by investment cycles. From 2010 to 2021, interest rates were low, allowing investors to fund growth at tech startups and biotech ventures. When interest rates increased in 2022 and 2023, investors began to look towards other investment opportunities, resulting in weaker job growth within tech and biotech. Now that interest rates are declining again, which is expected to carry through in 2025, investors are likely to reenter the tech and biotech sector, igniting a new round of hiring. Tech employment is expected to increase by 1.5 to 2.5% while biotech employment could expand by 1 to 2%.

Restaurant Growth Deceleration

Restaurants created more than 200,000 jobs in 2024, according to the U.S. Bureau of Labor Statistics, placing it among the fastest growing sectors. The post-pandemic consumer patterns shifted from an initial surge of goods purchases demand (due to lockdowns) to a rise in demand for services.

This is also part of a cultural mindset we refer to as “living for today,” which includes dining out, driving strong hiring trends at restaurants. However, household dining budgets peaked in 2024, and we anticipate some of this to reverse over the next few quarters. In fact, restaurant sales are beginning to flatten out and we expect restaurant hiring growth to slow in 2025.

Shift in Globalization, Not De-Globalization

Impact of Tariffs on Global Trade, U.S. Economic Growth, and Inflation

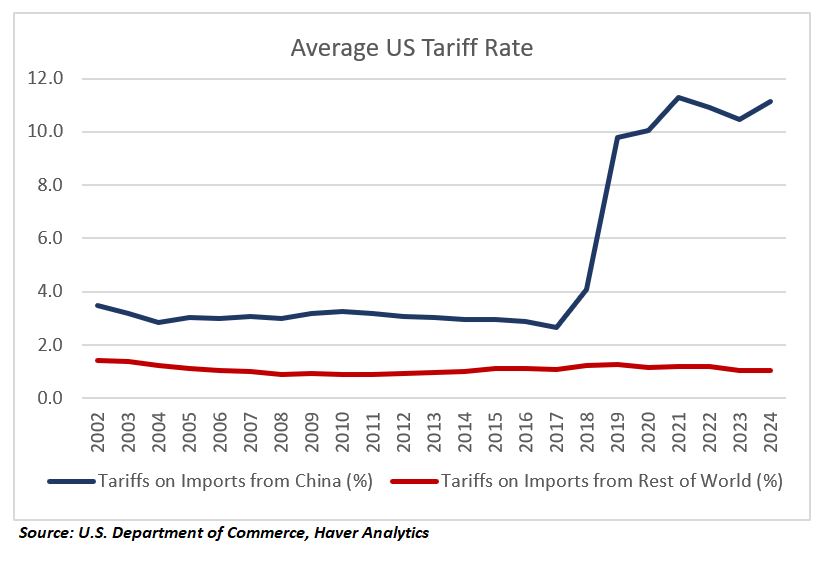

The use of tariffs has expanded in recent years following the placement of import duties on Chinese goods starting in 2018. Since then, the average tariff on Chinese products headed to the U.S. has quadrupled, reaching an average rate of around 11%. Looking ahead, we anticipate tariffs to become increasingly bipartisan; the main questions will be what tariff rates to set and on which countries and products.

Higher tariffs have already had meaningful economic impacts on U.S. trade. For example, U.S. imports from China as a percentage of all imports has fallen in recent years, whereas imports from Mexico, Vietnam and India have increased. Notably China’s overall exports have not declined much. Instead, Mexico’s imports from China have risen quite a bit, indicating that trade from China may be flowing through other markets. This could include a simple rerouting of goods, or the assembly and packaging of Chinese products in new markets, which are then reexported. If 2024 tariffs hold steady throughout 2025, shipping between China and Mexico could continue to rise alongside a pick-up in Mexico-U.S. cross border trucking traffic.

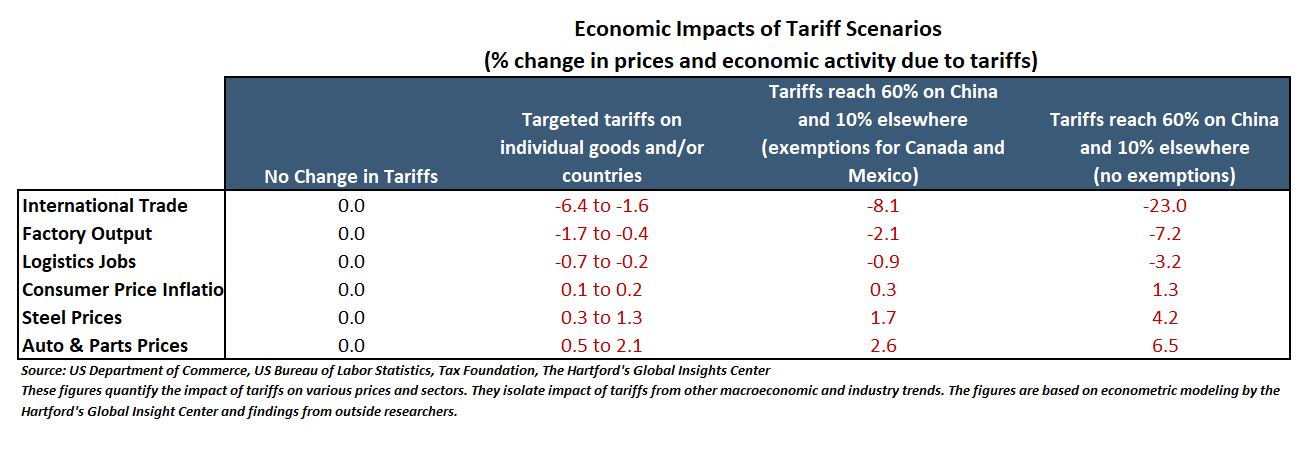

But what happens if tariffs continue to rise further as expected? The answer depends on how high tariffs advance.

Based on the Global Insights Center’s calculations, if tariffs increase slightly, then U.S. imports and exports could fall a bit, around 2.5% on average. But if the most extreme version of tariffs are implemented, then U.S. imports and exports could be hindered significantly and fall by 23%.

The base case expectation for 2025 is that global trade will continue to shift and we are set to see a transition in globalization, rather than de-globalization. However, if tariffs are increased aggressively, then de-globalization could indeed transpire.

Inflation and Interest Rates Set to Further “Normalize”

Inflation Moderation Expected, Allowing Lower Interest Rates

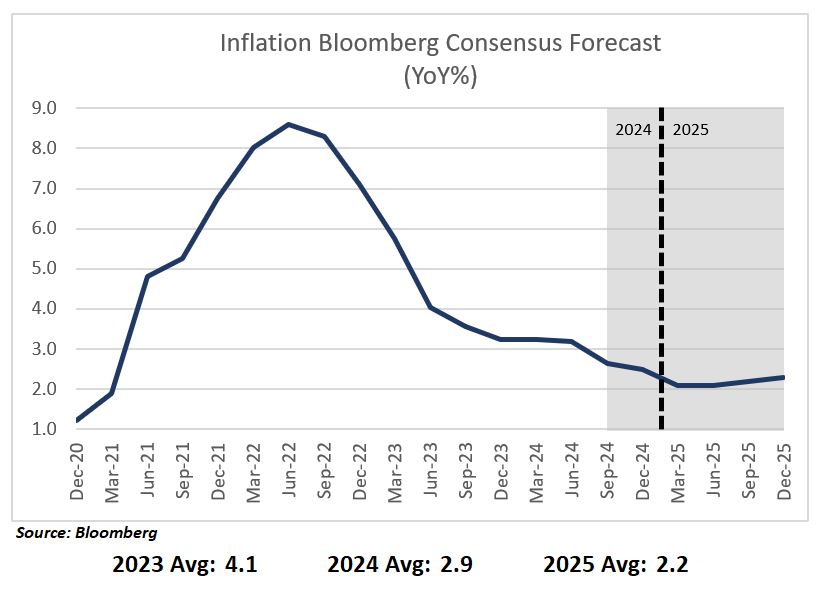

Inflation broadly normalized throughout 2024, despite some initial concerns that it would remain elevated (especially in the spring when headline inflation was stuck in the mid-3% range). At the Global Insights Center, we largely maintained throughout the year that inflation would fall to the mid-to-low 2% range by the end of 2024, and average 3% across the year. We also felt this would enable the Federal Reserve to cut interest rates at least once in the second half of the year. This mostly held true.

For a bit more context, inflation began to rise following COVID-19 and peaked at 9.1% in 2022. Inflationary pressures increased initially due to rising goods prices. Goods prices increased because output from Asia was curtailed due to factory shutdowns; the shipping sector was dislocated, hindering the movement of goods; labor at ports were under strain, affecting the ability to unload ships with goods; and domestic demand in the U.S. increased because individuals stayed home and purchased goods instead of services. As those trends began to reverse, services inflation began to rise. In response, the Fed began to raise interest rates. But with inflation declining in 2024, the Fed started an interest rate easing cycle in September 2024.

For 2025, we expect inflation to continue to improve, even if a few months exhibit a bit of choppiness. Overall, inflation is likely to settle between 2% and 2.5%, enabling the Fed to continue to cut interest rates. As of now, market expectations are looking for the Fed Funds Rate to harmonize around 3.5% in late 2025. In contrast to prior years when interest rates were kept low—at times close to 0%—the Fed is expected to keep an elevated “terminal” rate this time. That way, if an economic crisis emerges, the Fed can react but cutting rates further. Notably, 3.5% is roughly the average interest rate of the past 40 years, so the Fed is expected to trend back to its long-term average interest rate.

Risks to the Inflation Outlook

The next question is how geopolitics, trade or other factors could influence inflation.

Geopolitics could affect U.S. inflation, but it depends on the severity of potential geopolitical flashpoints. Traditionally, tensions in the Middle East caused oil prices to rise. But over the past year, despite ongoing worries in the Middle East, oil prices actually declined.

How could that be? We believe that the answer is partially rooted in increased U.S. energy independence. The U.S. is the world’s largest oil consumer, and it’s also now the world’s largest oil producer. The vast majority of the oil used by Americans comes from domestic sources, followed by Canada and Mexico. As a result, the U.S. is not dependent on the Middle East any longer, which has perhaps resulted in energy prices becoming delinked from Middle East turmoil. This of course erodes the impact on U.S. energy inflation. With that said, a much larger conflict, or a material disruption to oil supplies outside the U.S. due to a regional war, could of course result in higher oil prices and thereby create inflationary risks to the U.S.

Trade flows are another area of risk. If additional (and significantly higher) tariffs are imposed on goods coming in from all countries and covering all products, it’s likely that the price of imported goods would rise while domestic production faces headwinds. These developments could cause some upward pressure on overall inflation.

Lower Rates Could Impact Manufacturing, Housing Construction, Tech, Auto Sales

If interest rates continue to decline in 2025, they are likely to support growth in manufacturing, housing construction, tech and auto sales.

Manufacturing activity is sensitive to interest rates because factory output is skewed towards big-ticket items, like autos and airplanes, and high interest rates lead to lower demand for these products. Factory equipment is also expensive to buy and repair, so manufacturing plants often use loans and credit to purchase and maintain their machinery.

Manufacturing activity has been on pause for almost three years, weighed down by high rates. If rates fall as we expect, manufacturing could enter a new growth phase in 2025 and beyond. In general, we remain positive on the advanced manufacturing sector due to geopolitics. AI will continue to be a focal point for the U.S. government as nations seek to harness this evolving technology. In light of that, we expect continued focus on developing semiconductor facilities, data centers and fiber optic networks within the U.S. This will also necessitate more investments in advanced energy development. As this geopolitical need meets a lower interest rate environment, we expect an uptick in capital expenditure in these verticals.

Interest rates also significantly impact tech because the industry relies on capital financing to operate and grow. From 2010 to 2021, when interest rates were very low, investors placed high volumes of capital into tech startups since capital was “cheap” and there was promising upside from tech firms that did well. But when interest rates increased, investors were not able to borrow as cheaply. Many began to prioritize alternative high-yielding investment options. Accordingly, a pending lower-rate environment could unlock a new wave of tech startups that create jobs and boost the economy in the coming year.

Auto sales have been sluggish for several years. Before the pandemic, when the economy was performing well and when interest rates were lower, Americans bought 16.5 million to 17.5 million autos per year. In 2023, that figure declined to 15.6 million vehicles, in part because of elevated auto loan rates. Due to the softening in auto sales, wage growth for auto dealers has been weak. Lower rates could help lift auto sales back to their pre-pandemic range.

Lower interest rates could also support broad-based consumer spending. The American consumer spent surprisingly freely in 2022 and 2023 despite high interest rates, and consumer activity was a major tailwind for the economy. If the Fed cuts interest rates like we expect, it could lead to lower rates for credit cards, auto loans and others that directly impact household budgets. Lower interest expenses could also prolong the current free spending atmosphere. After consumer spending increased 2.5% in 2023 and trended towards 2.7% in 2024, it could expand 2.5 to 3.5% in 2025.

Lower interest rates could also support broad-based consumer spending. The American consumer spent surprisingly freely in 2022 and 2023 despite high interest rates, and consumer activity was a major tailwind for the economy. If the Fed cuts interest rates like we expect, it could lead to lower rates for credit cards, auto loans and others that directly impact household budgets. Lower interest expenses could also prolong the current free spending atmosphere. After consumer spending increased 2.5% in 2023 and trended towards 2.7% in 2024, it could expand 2.5 to 3.5% in 2025.

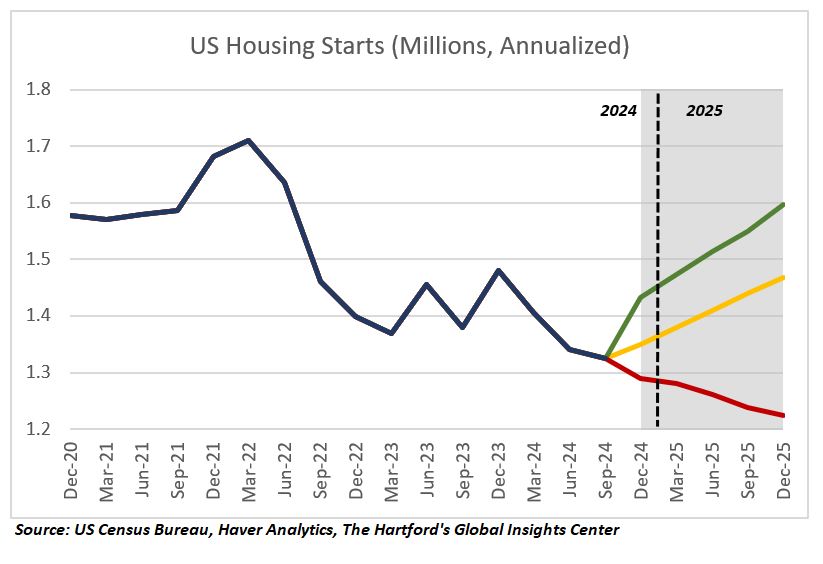

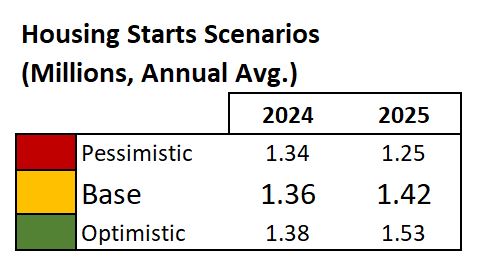

Lower interest rates could also boost housing demand, spurring builders to ramp up construction. Like manufacturing, the housing market slowed down when interest rates increased over the last few years. Higher rates made mortgages more expensive and many buyers left the market, so builders pulled back. If rates fall, mortgages could become cheaper and more people could buy homes. Under this outlook, builders would likely increase production. We expect construction to begin on 1.42 million homes and multifamily units in 2025, up from 1.36 million in 2024.

Lower interest rates could also boost housing demand, spurring builders to ramp up construction. Like manufacturing, the housing market slowed down when interest rates increased over the last few years. Higher rates made mortgages more expensive and many buyers left the market, so builders pulled back. If rates fall, mortgages could become cheaper and more people could buy homes. Under this outlook, builders would likely increase production. We expect construction to begin on 1.42 million homes and multifamily units in 2025, up from 1.36 million in 2024.

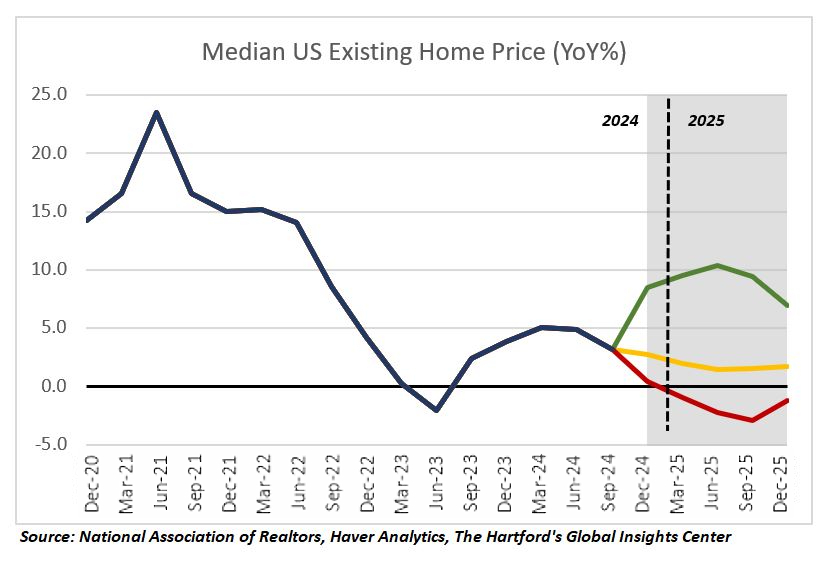

U.S. Housing Market Transactions May Pick Up

Lower Rates Could Spur Demand, Ease Supply Constraints

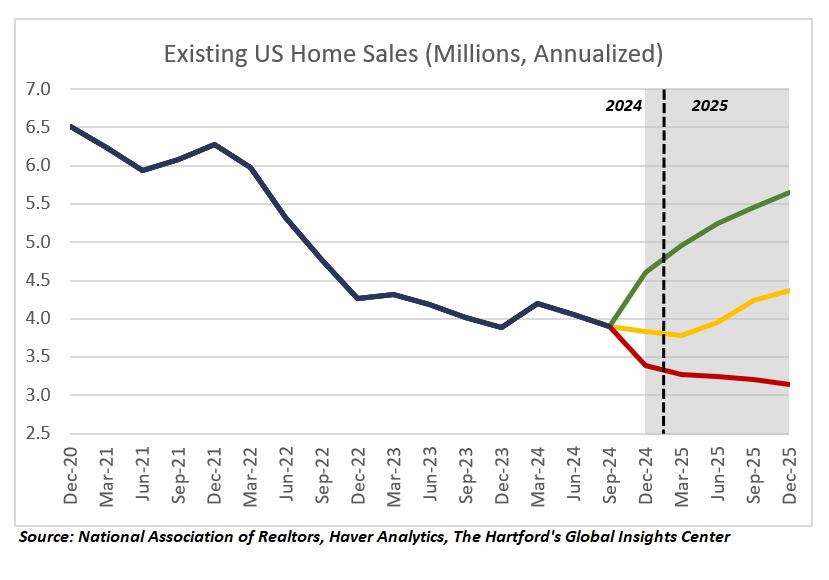

U.S. home sales volumes are likely to gain traction by mid-2025 as mortgage rates are expected to decline. When interest rates increased and the 30-year fixed mortgage was elevated, demand for homes naturally declined. So, too, did the number of existing homes for sale on the market. In September 2024, just as the Fed began to ease interest rates, the inventory of unsold existing homes stood at 1.39 million units, amounting to 4.3 months’ supply. Anything below 5-6 months of supply indicates tight conditions with low inventory.

This happened because would-be sellers of existing properties were on the sidelines. Many did not want to sell because they likely locked in a low mortgage rate in prior years and would have had to take on a higher interest rate in a new home purchase. With minimal homes on the market, existing home sales were on track to decline 2.6% as of late 2024. As interest rates decline, though, some would-be sellers may start to put their homes on the market, thereby helping ease supply constraints in this segment.

The new home market, meanwhile, had elevated inventory levels. In the same month of September 2024, inventory of new homes stood at 470,000 unsold units, amounting to 7.6 months’ supply, close to the highest on record. Anything above 5 to 6 months indicates the market is oversupplied. With ample units on the market, sales transactions for new homes were on pace to grow 6.2% as of late 2024.

Now that interest rates are poised to decline, we anticipate a loosening of the housing market (especially for existing homes), resulting in increased transaction volumes for new and existing homes. The shift may not be immediate because there is a lag between when the Fed starts to cut rates and when fixed rate mortgage products begin to come down.

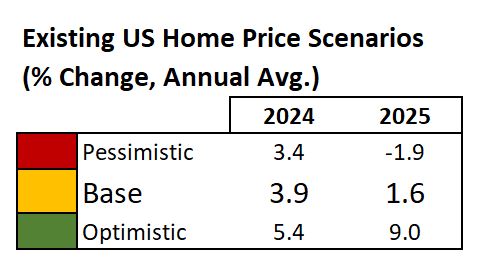

While we anticipate transactions to pick up in the coming year, we expect home prices to increase very slowly. Housing affordability is a challenge for most families, keeping potential buyers on the sidelines and preventing home prices from rising quickly.

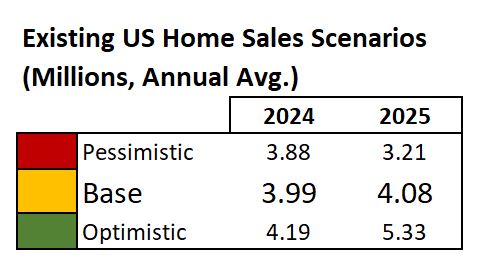

Based on the Global Insight Center’s econometric model, existing home sales are expected to reach 4.08 million transactions in 2025, up from 3.99 million in 2024. The median existing home price is likely to increase by 1.6% compared to 3.9% the year prior. Sales transactions of new homes could reach 773,000 in 2025, up from 707,000 previously.

Performance Expected to Remain Mixed

Growth May Remain Sluggish in Europe and U.K.

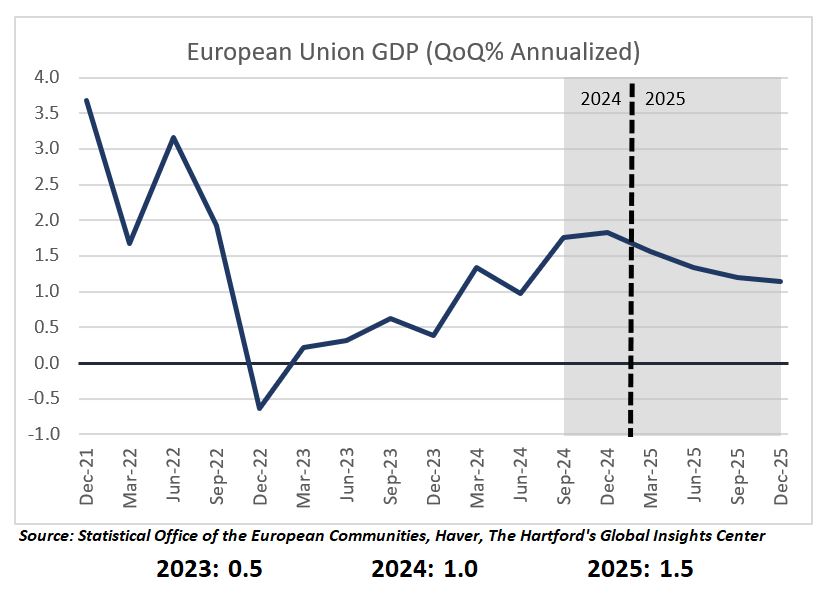

Economic growth in the European Union will likely remain mixed again in 2025 as various headwinds may persist, in particular for core industrial economies such as Germany.

However, markets such as Spain may remain relatively strong. We anticipate the aggregate economic zone will struggle to maintain growth momentum, and our model suggests tepid expansion throughout 2025, with GDP growth averaging 1.5% across the block.

Germany, the largest EU economy, could end 2024 in a technical recession that may prove difficult to exit in 2025. The business climate remains challenged with manufacturing companies noticeably pessimistic about current and future conditions. Germany was heavily dependent on Russian natural gas in the run up to the war in Ukraine, and only made itself more so by shutting down nuclear power in the decade prior. Energy intensive industries continue to lag other manufacturers, which weighs on general economic performance.

Another factor weighing on the German economy is an aging population. Approximately 25% of Germany’s total population is 67 or older, which is considered the state retirement age. The country is trying to attract younger skilled labor and has taken some legislative initiatives such as the 2023 Skilled Immigration Act and the 2024 New Citizenship Law. Both pieces of legislation are designed to ease the immigration process and provide a faster track to German citizenship while allowing immigrants to retain their original citizenships, a change from previous requirements to only hold German citizenship.

Italy is also under pressure, with Italian manufacturers facing slowing demand across the board and negative sentiment coming from the industry’s close ties to Germany. Weak confidence and lingering energy related challenges suggest an industrial sector turnaround in 2025 is unlikely.

Meanwhile, EU periphery economies like Spain should be noticeably healthier in 2025, as peripheral service dependent economies outpace the core industrial nations. For example, tourist overnight stays in Spain reached an all-time high in the summer of 2024, beating the previous record set before the COVID-19 pandemic. This has sparked some backlash protests from locals that are unhappy with the impact tourists have on local infrastructure and consumer prices, but similar protests occurred in prior eras and did not have lasting economic impacts.

Across the EU, like the economy in general, the jobs market is rather bifurcated with weakness in manufacturing and strength in service-related roles. The EU should finish 2024 with an overall unemployment rate around 6%, but it could rise to 6.1% over the course of 2025. While Germany’s unemployment rate is relatively stagnant at 6%, Spain’s service focused jobs market has had a strong comeback from the pandemic, enabling unemployment to fall from 26.4% in 2013 to around 11% in 2024.

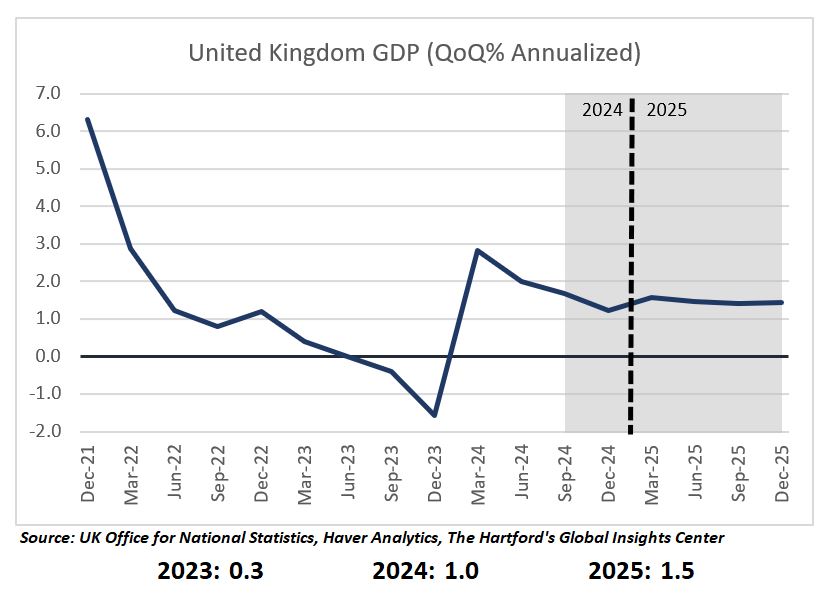

For the United Kingdom, we similarly expect GDP growth to average 1.5% in 2025. The U.K. service industries are now making a material contribution to domestic economic expansion, and household spending should start to support economic activity more meaningfully in the year ahead, especially if the unemployment rate levels off at around 4.5%, as we expect.

Additionally, the new government in the U.K. has indicated it may seek to improve its trading relationship with the EU, which was complicated following Brexit. Any improvement here should provide a boost to jobs.

Moderating Consumer Price Inflation and Easing Central Bank Policy

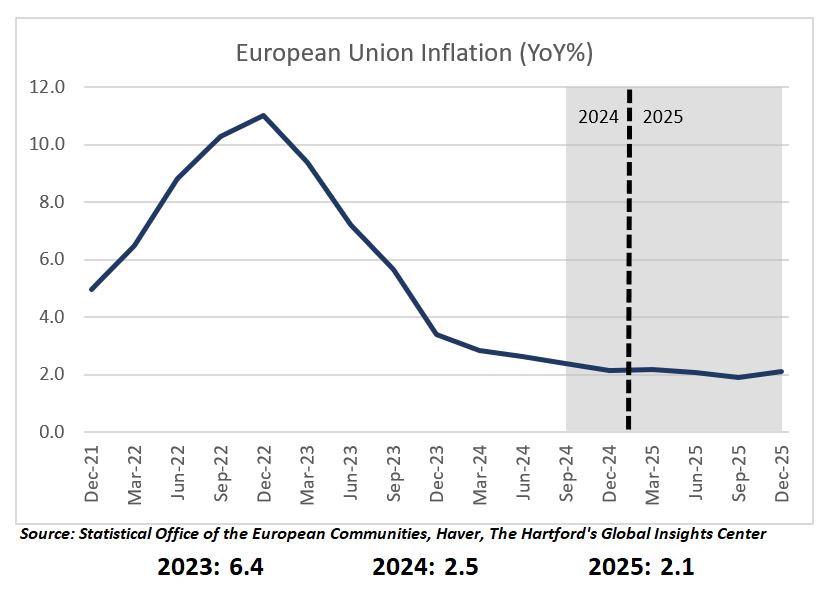

Throughout 2024, inflation in the EU and the U.K. normalized, falling close to the 2% target in the fourth quarter. In 2025, inflation should continue to moderate with problem areas, such as services, normalizing as well. Overall, we anticipate EU inflation averaging 2.1% in 2025. With inflation coming under control, the European Central Bank should be able to cut interest rates to around 3% by the end of 2025 from 4.5% at the start of 2024.

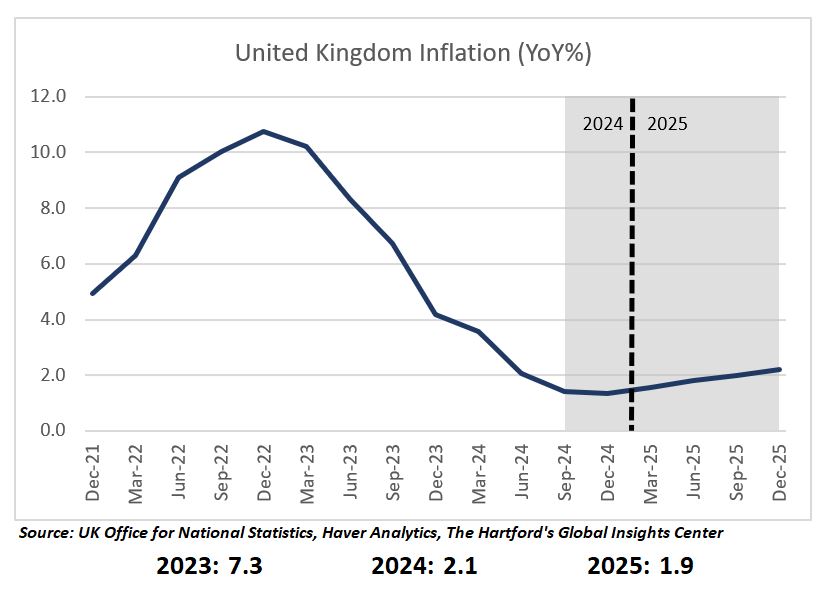

In the U.K., inflation fell below the Bank of England’s 2% target in 2024 largely due to moderating energy prices. We anticipate though that inflation could rise slightly in 2025 due to domestic cost pressure and an uptick in household energy bills as the regulator adjusts price caps, though it is expected to average just 1.9%. Similar to Europe, goods inflation in the U.K. has moderated while services inflation remains a problem from high wages.

The U.K. has the added challenge of labor shortages in its economy that are likely to persist in 2025. Nonetheless, the Bank of England is expected to follow other central banks around the world and reduce the official bank rate to around 4% by the end of 2025 from 5.25% at the start of 2024.

The U.K. has the added challenge of labor shortages in its economy that are likely to persist in 2025. Nonetheless, the Bank of England is expected to follow other central banks around the world and reduce the official bank rate to around 4% by the end of 2025 from 5.25% at the start of 2024.

This article provides general information, and every effort has been made to ensure accuracy of the information contained herein. In no event will The Hartford be liable for direct, special, incidental, or consequential damages (including, without limitation, damages for loss of business profits, business interruption, loss of business information or other pecuniary loss) arising directly or indirectly from the use of (or failure to use) or reliance on the information contained herein, even if The Hartford has been advised of the possibility that such damages may arise.

Links from this site to an external site, unaffiliated with The Hartford, may be provided for users' convenience only. The Hartford does not control or review these sites nor does the provision of any link imply an endorsement or association of such non-Hartford sites. The Hartford is not responsible for and makes no representation or warranty regarding the contents, completeness or accuracy or security of any materials on such sites. If you decide to access such non-Hartford sites, you do so at your own risk.

The Hartford Insurance Group, Inc., (NYSE: HIG) operates through its subsidiaries, including the underwriting company Hartford Fire insurance Company, under the brand name, The Hartford,® and is headquartered in Hartford, CT. For additional details, please read The Hartford’s legal notice at https://www.thehartford.com.